Because of how it has some running costs associated with it and how its value depreciates as soon as you drive it off the lot, your car is traditionally referred to as a liability instead of an asset, certainly as far as the financial sector goes at least. So although from a financial stand-point your vehicle is indeed a liability, depending on what you use it for, you can functionally refer to it as an asset instead of the liability it really is.

It’s as simple as taking into account considerations such as how certain areas of your life would be like had you not had access to your car. For example, would you be at greater risk of being late for work if you had to take the tube instead? Would you be able to complete certain errands which form part of what your job is all about?

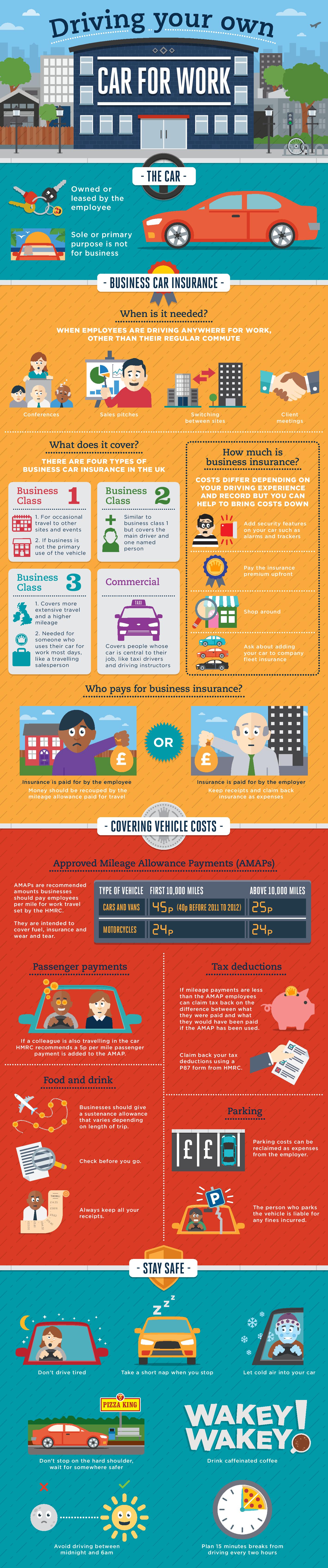

Do you perhaps run a business, much like the many transport industry business ideas which exist around the vibrant Ford Focus leasing market (like moonlighting as an Uber driver)? Do you drive your car to attend sales pitches, networking sessions and seminars of which your attendance was commissioned by your employers?

These questions naturally all form around the relationship between the manner in which you use your car and your workplace, which is important to consider because that’s essentially what turns what would ordinarily be a liability into an asset. Now, while this has some direct implications to your personal finances and savings, it perhaps has even greater implications to the insurance covering your vehicle, albeit in a way that is suggestively indirect.

As indirect as it may be, it’s very important nevertheless, because it could make for the difference between meeting the requirements to qualify for a payout if you need to file and claim, and being refused on grounds of the technicalities involved. Basically you can’t just drive your own car for work purposes other than driving to work without it complicating the insurance required to cover it a bit.

Of course I use the word “complicate” rather loosely and I can see why it might be a bit of an overstatement, but that’s just to emphasise the importance of taking into account the fact that you’ll need different insurance to that of just personal auto insurance if you do indeed use your own vehicle for work-related purposes.

This applies to any car which you own outright or indeed if you’ve taken out something like a leasing contract. The dynamics and finer details around the issues which need attention will indeed be what ultimately determine the class of insurance you’ll need added to cover your vehicle, but the bottom line is that your personal auto insurance will no longer suffice on its own.